In our first series on ingredient price movement, we looked at a category (Chocolate) that experienced very high rates of inflation while maintaining its sales volume and consumer base. In this release, we will look at whey and plant protein within the larger Protein Supplement & Meal Replacement Subcategories.

Why? Because over the past two years, the underlying economics of whey protein have shifted meaningfully; commodity inputs, supply chain capacity, and consumer demand converge to create structural disconnects that flow through to shelf price changes. Doing a deep dive into this ingredient deepens our understanding of the connection between macroeconomic movement and our industry.

Additional context to consider:

- The price of U.S. whey protein concentrate (WPC 34%), a key formulation benchmark, has moved up from recent cyclical lows, reflecting tighter inventories, limited spot availability, and sustained demand (1,2).

- Higher up the protein value chain, WPC 80 and whey protein isolate continue to experience tighter processing capacity and strong demand for high-purity proteins tied to performance nutrition and everyday protein consumption (2,3).

Market Pricing

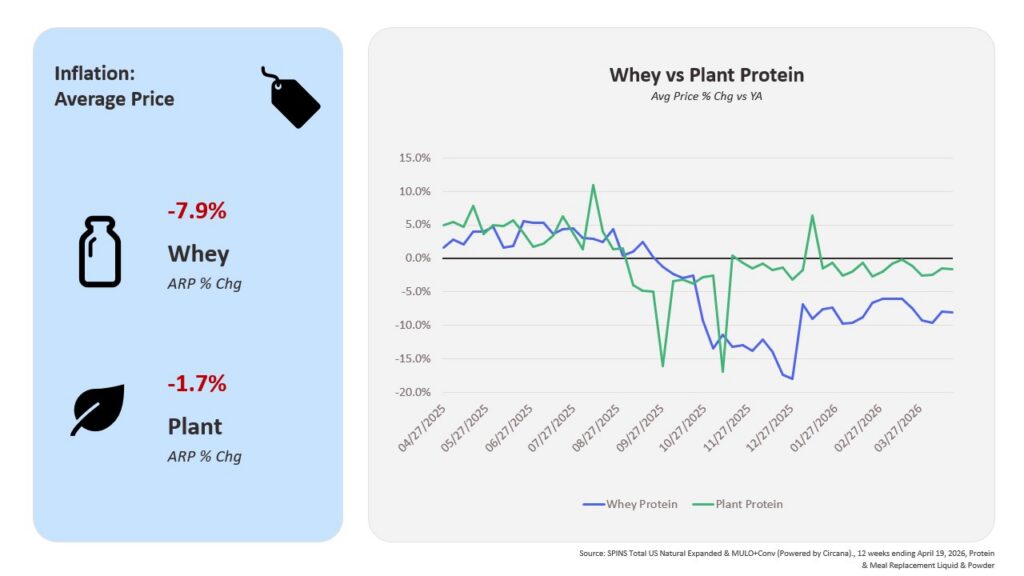

The average price for products containing whey protein and plant protein (respectively) declined versus the previous year, though the magnitude and drivers differ significantly between segments. Products with whey protein average retail price declined 7.9% versus the previous year, while products with plant protein prices declined a more modest 1.7%.

Exhibit 1:

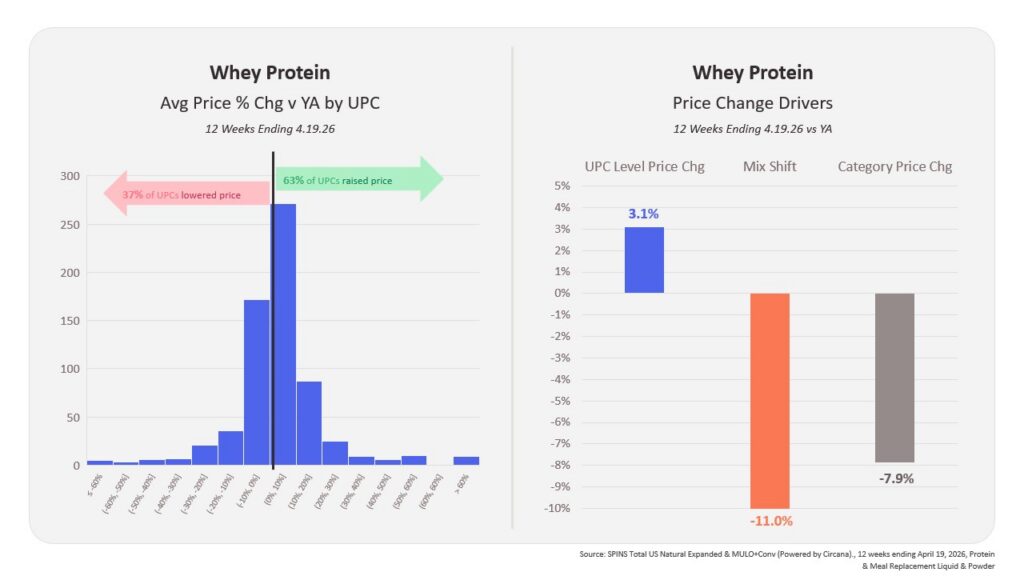

Despite category-wide prices declining for whey protein, the majority (63%) of whey protein UPCs raised prices, with an average increase of 3.1%. The decline in category-wide price is driven most by a shifting mix to lower-priced items, both from more mid-tier brands growing at a faster rate than ultra-premium brands, and from premium brands introducing more single-serve options. In fact, close to 50% of the unit growth in whey protein came from items that are $5 or less.

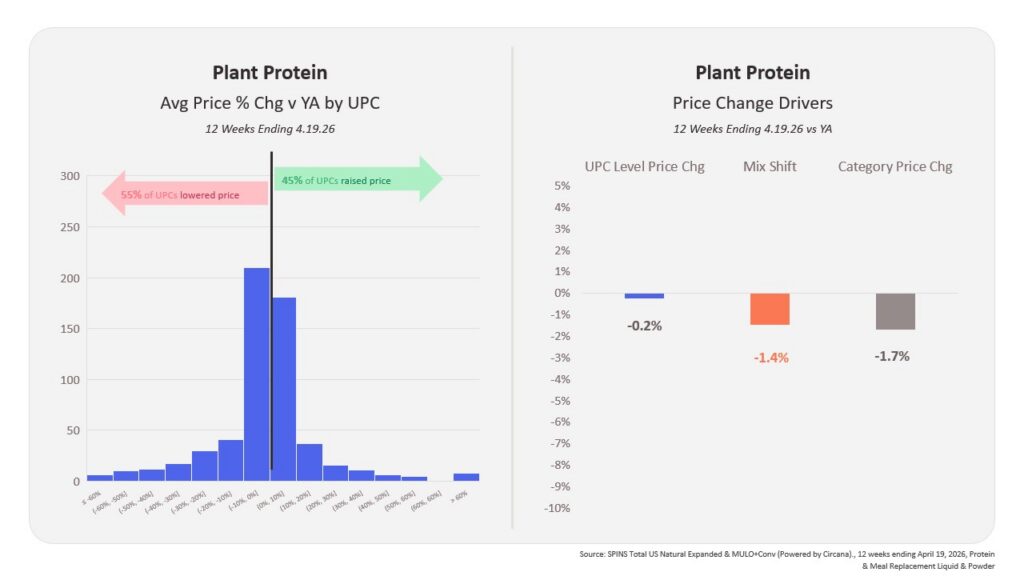

Plant protein UPC pricing was comparatively more stable. While many products also reduced price, the overall segment had smaller category-level price movement.

Exhibit 2: Whey Protein

Exhibit 3: Plant Protein

Exhibit 3: Plant Protein

Demand Impact

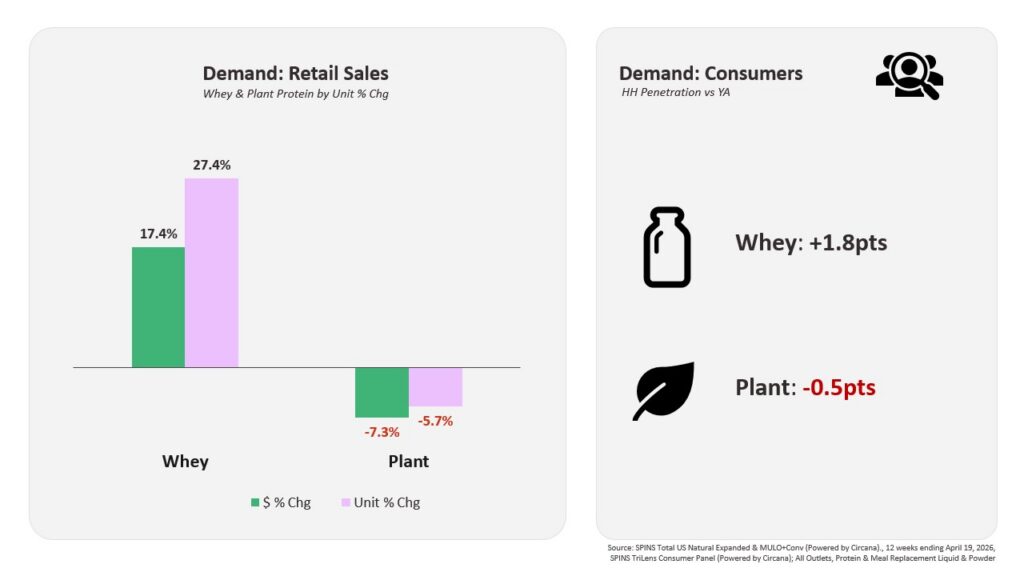

Consumer demand trends sharply diverged between whey and plant protein. Whey protein continued strong growth, with dollar sales increasing 17.4% and unit sales increasing 27.4% versus the previous year. Household penetration for whey protein also increased by 1.8 points, demonstrating continued consumer engagement and broad-based demand growth.

Plant protein, however, experienced declining demand despite stable pricing. Dollar sales declined 7.3% while unit sales fell 5.7% versus the previous year. Household penetration also declined by 0.5 points, indicating that fewer consumers are purchasing the segment.

Exhibit 4:

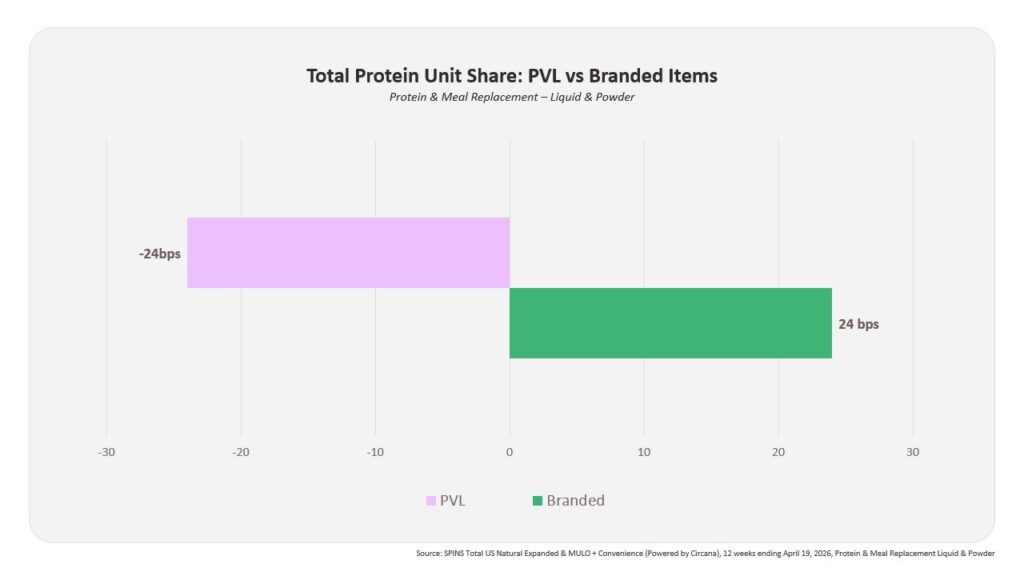

Shopper Response & Value Dynamics

Despite the shifting mix to lower-priced items that we see in both whey and plant protein, consumers are not responding to higher prices by trading all the way down to the lowest-priced options. Branded Protein items gained share versus Private Label products, with Branded items increasing 24 basis points in dollar share during the latest 12-week period.

While both whey and plant protein products experienced some degree of pricing adjustment, products with whey protein are significantly more resilient, driving category growth and attracting new shoppers.

Exhibit 5:

Hidden pricing pressure in a high-demand category

Overall, the Protein category demonstrates how consumers make tradeoffs when faced with rising costs. Protein as a nutrient is in high demand, and while that creates a significant tailwind for the Protein Supplement Categories, the shift in product mix to lower-priced options helps a category maintain strong growth and bring in more new households.

While SPINS retail data shows whey protein prices declining at the shelf, down 7.9% year-over-year, largely due to mix shifts toward lower-priced formats and increased presence of value-tier offerings, the upstream system signals mounting cost pressure that has yet to fully flow through. The data suggests that future price increases are likely, forcing brands to reconsider formulation strategies, ingredient blends, and margin trade-offs. At the same time, consumer demand for protein remains exceptionally strong, which will likely manifest not as demand destruction but as trading across channels, brands, and protein sources as shoppers seek to maintain protein intake while managing value.

Downloadable Chart Pack

Access the individual slides shown in this post — formatted and ready to use in your own presentations.

Works Cited

- CLAL. World: Price of Whey Protein Concentrate (WPC), export and U.S. benchmarks, 2024–2026 trends.

- USDA Agricultural Marketing Service (AMS). Dairy Market News – Whey Protein Concentrate (Central & West U.S.), May 2026 (includes WPC 34 pricing trends and market commentary, with reported WPC 80 spot context).

- ENZBio. Global Whey Protein Pricing Overview (Concentrate vs. Isolate), 2025–2026.

- SPINS Total US Natural Expanded & MULO+Conv (Powered by Circana). Protein Price Tracker Brief, 12 weeks ending April 19, 2026.