Market Pricing

Olive oil’s recent price volatility offers a powerful case study on how multiple economic forces, including those related to extreme weather and agricultural constraints, can reshape even the most established food categories.

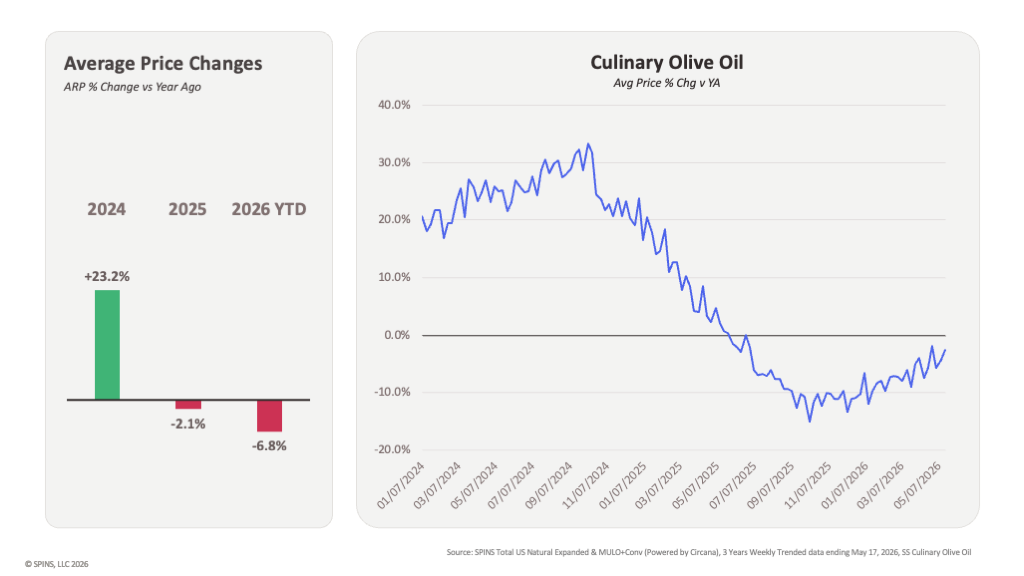

Historically viewed as a relatively stable pantry staple, years of droughts and extreme temperatures across the Mediterranean, particularly in Spain, which accounts for roughly 40% of global olive oil production, drove significant supply shortages, pushing olive oil prices to record highs (1). By 2024, average oil prices rose approximately 23% versus the prior year (see Exhibit 1).

Exhibit 1:

Olive oil’s recent pricing swings highlight a growing challenge across food & beverage categories, as environmental disruptions can quickly translate into supply shortages and cost inflation. As climate variability increases, categories that are dependent on agricultural goods may face similar pricing pressures.

Just as climate-related disruptions drove olive oil prices up, improved growing conditions helped reverse this trend. Stronger harvests increased global supply and eased market pressures (2). While olive oil prices remained elevated relative to historical levels, price increases began to decline in 2025 (-2% vs 2024). In 2026 to date, prices have further reduced by nearly -7%.

Demand Impact

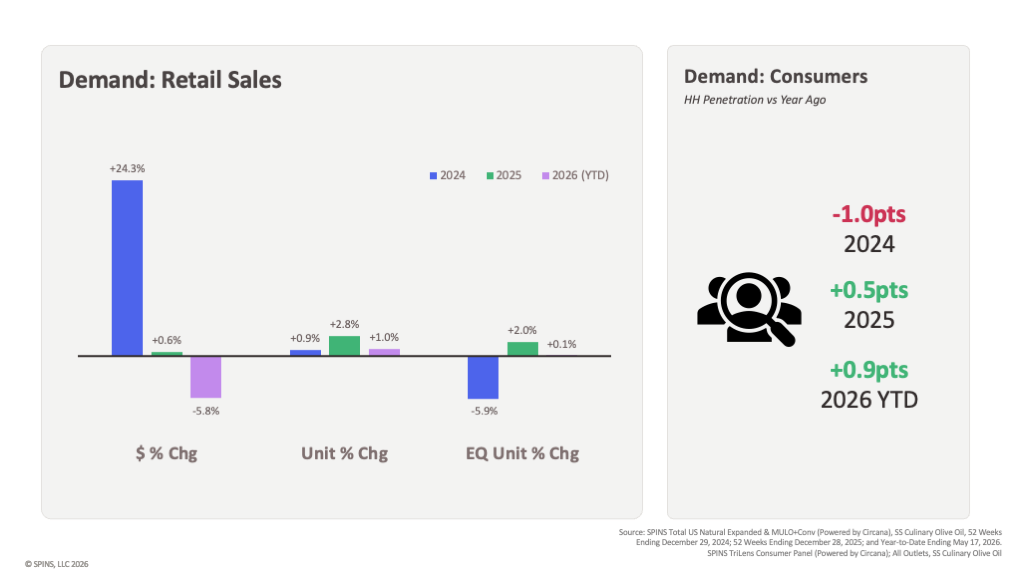

While olive oil prices have experienced significant volatility over the past several years, underlying demand has proved resilient. Retail dollars surged 24% in 2024 (see Exhibit 2), while unit sales remained relatively stable (+0.9%). Consumers did, however, adapt their purchasing behavior. Equivalent unit sales declined nearly 6%, as some shoppers reduced purchase quantities and/or opted for smaller sizes to help offset the impact of higher prices. A slight decline in household penetration (-1.0pts) further indicates that some consumers temporarily exited the category during this period of peak pricing.

Exhibit 2:

As supply conditions improved and pricing pressures eased in 2025, these behaviors began to reverse. Household penetration increased (+0.5pts), indicating that some consumers returned to the category, while unit sales grew +2.8% YoY. Equivalent unit sales also returned to growth (+2.0%), as prices softened.

Together, these trends suggest that while pricing volatility of olive oil significantly affected consumer spending, its impact on underlying demand was more limited. Rather than find a permanent substitute, consumers adjusted purchasing behavior by reducing quantities, purchasing smaller sizes, or temporarily exiting the category. As pricing pressures eased, both purchasing behavior and household penetration began to rebound, reinforcing olive oil’s position as a staple ingredient rather than a discretionary purchase.

More broadly, the olive oil category demonstrates that consumers do not always respond to inflation by abandoning a product entirely. Instead, they are likely to adapt their purchasing behavior for goods perceived as essential to their health and everyday life.

Premiumization Despite Pricing Peaks

While supply disruptions were a primary driver of olive oil’s pricing increases, it was not the only factor influencing category growth. At the same time, consumer preferences within the category were evolving, as shoppers increasingly viewed olive oil as being associated with health, quality, ingredient transparency, and overall culinary experiences.

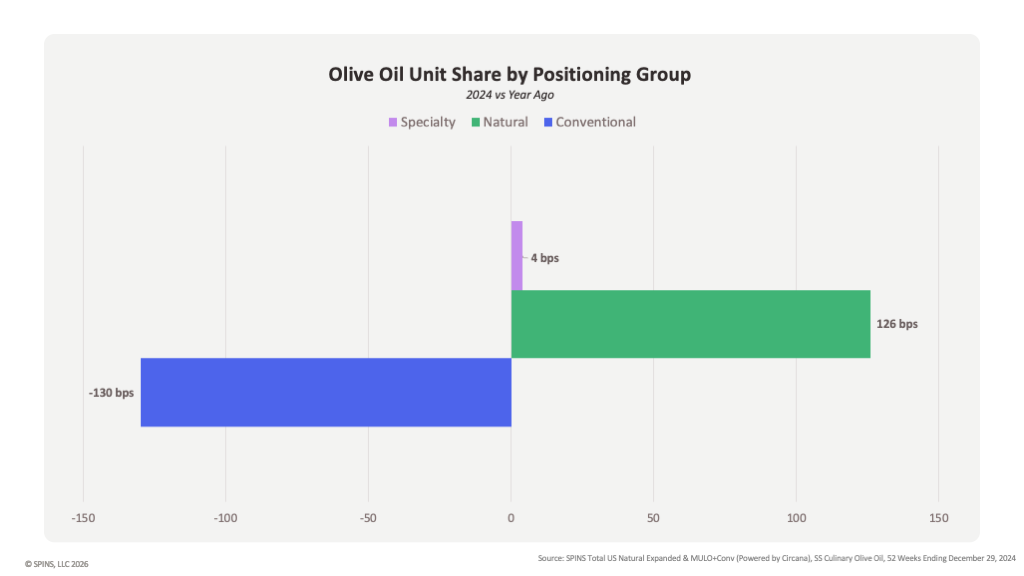

This shift is reflected in the category’s positioning dynamics. In 2024, natural-positioned olive oils gained 126 basis points of unit share, while conventional lost 130 basis points (see Exhibit 3).

Exhibit 3:

Despite record-high pricing, consumers continued to gravitate towards products that aligned with wellness, quality, and ingredient transparency, showcasing that purchasing decisions were influenced by factors beyond price alone.

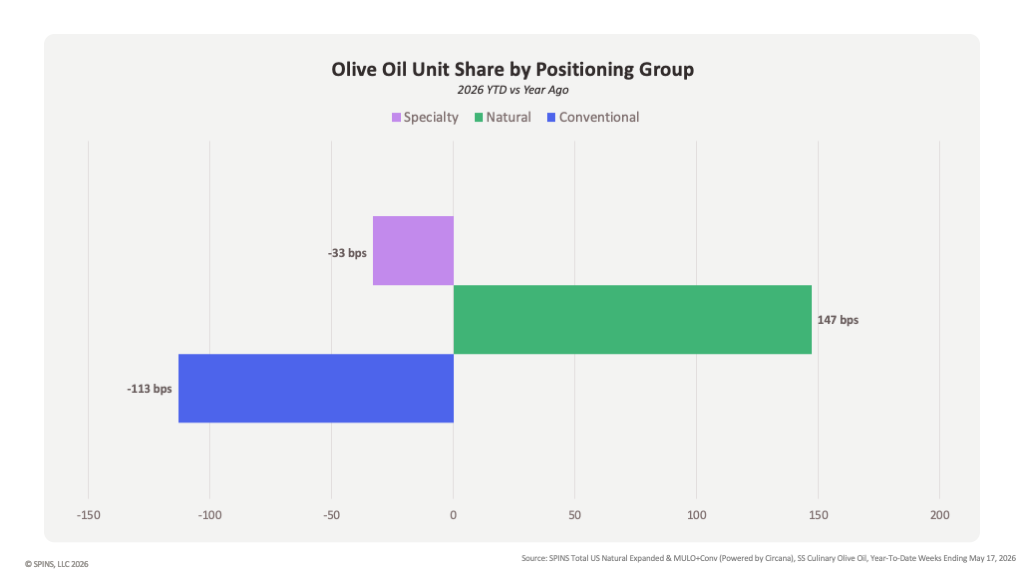

This trend has persisted even as olive oil prices have settled. In 2026 YTD, natural-positioned olive oils gained an additional 147 basis points of unit share, while conventional products continue to lose share (see Exhibit 4).

Exhibit 4:

The sustained growth of natural offerings demonstrates that in certain food & beverage categories, consumer interest in premium options continues even as inflationary pressure pushes prices up to historic levels.

Looking Ahead

Olive oil’s recent market dynamics demonstrate how changing consumer preferences can reshape the pricing dynamics of a category despite supply chain disruptions. While supply disruptions drove significant pricing volatility, consumer demand remained resilient in the long term, and natural-positioned olive oils continued to gain share. The category’s performance suggests consumers are willing to adapt to higher prices for products they view as staples in everyday cooking and essential to health and quality.

Looking ahead, olive oil will likely continue to benefit from broader shifts in consumer behavior. As pricing continues to normalize from 2024 peaks, growing interest in health-focused products and growing negative perception of seed oils provide strong tailwinds for the category.

The underlying dynamics of the olive oil market are relevant across the food industry. Categories that are highly tied to agriculture may face greater pricing volatility, especially if climate-related disruptions become more common. While olive oil was able to rebound from its sales volume declines and maintain growth in natural-positioned products, not every category with rapid inflation experiences the same outcome. Understanding how consumers value specific goods and adapt during periods of pricing peaks will become increasingly important for brands.

Downloadable Chart Pack

Access the individual slides shown in this post — formatted and ready to use in your own presentations.

Works Cited

- Columbia Climate School. As Climate Change Exacerbates Extreme Weather, Olive Oil Feels the Squeeze. March 24, 2026.

- Spain’s Deoleo says olive oil prices set to halve from record levels. November 15, 2024.