Overview

From Niche to Framework

Conscious Consumption – the driving ethos for discovery, purchase, and brand loyalty among food and beverage shoppers – is now the dominant framework driving $350 billion in annual sales in the US. Price remains a critical factor, but it is now filtered through increasingly non-negotiable values comprised of ingredient integrity, transparency, and ethical impact. Our data confirms this is not a cyclical trend, but rather a structural shift—the “Values-Oriented Shopper” is no longer a niche participant but rather an active catalyst of growth in every category.

Context & Methodology

In January 2026, SPINS fielded a brief survey to consumers representative of the American population. The survey aimed to assess how consumers shop, how they discover products, and what drives their purchasing decisions.

The New Standard of Scale

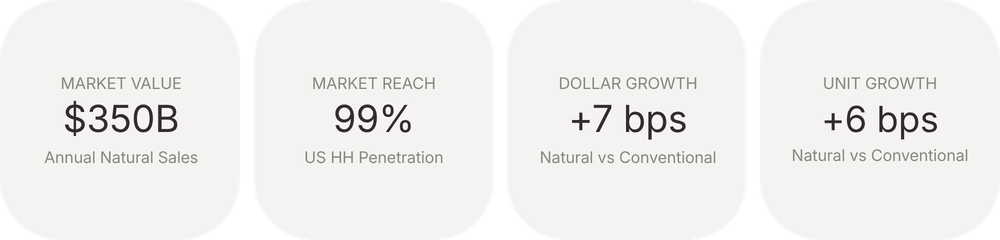

The natural products industry has evolved from a destination for a niche segment of enthusiasts in the 1960s and 70s into the CPG industry’s Gold Standard for quality, wellness, and innovation. Data from the SPINS TriLens Consumer Panel proves the barrier to entry has dissolved: 99% of U.S. households purchased at least one natural product in the last 52 weeks.

This engagement is driving measurable velocity at the shelf. While conventional goods maintain volume dominance, the momentum has decisively shifted to natural products, which are outpacing conventional counterparts across each of these key growth metrics:

- Frequency: Natural product trips per buyer increased by 6% YoY.

- Basket Size: Shoppers spent 3% more per trip.

- Net Impact: These behaviors drove nearly 10% growth in dollar sales and a 7% increase in units sold.

Part I: The Divergence of Intent

Financial Sentiment as a Demographic

While values provide the framework, financial sentiment dictates the execution. We are seeing a sharp bifurcation in basket architecture, creating two distinct behavioral economies: the Confident Curator and the Constrained Strategist.

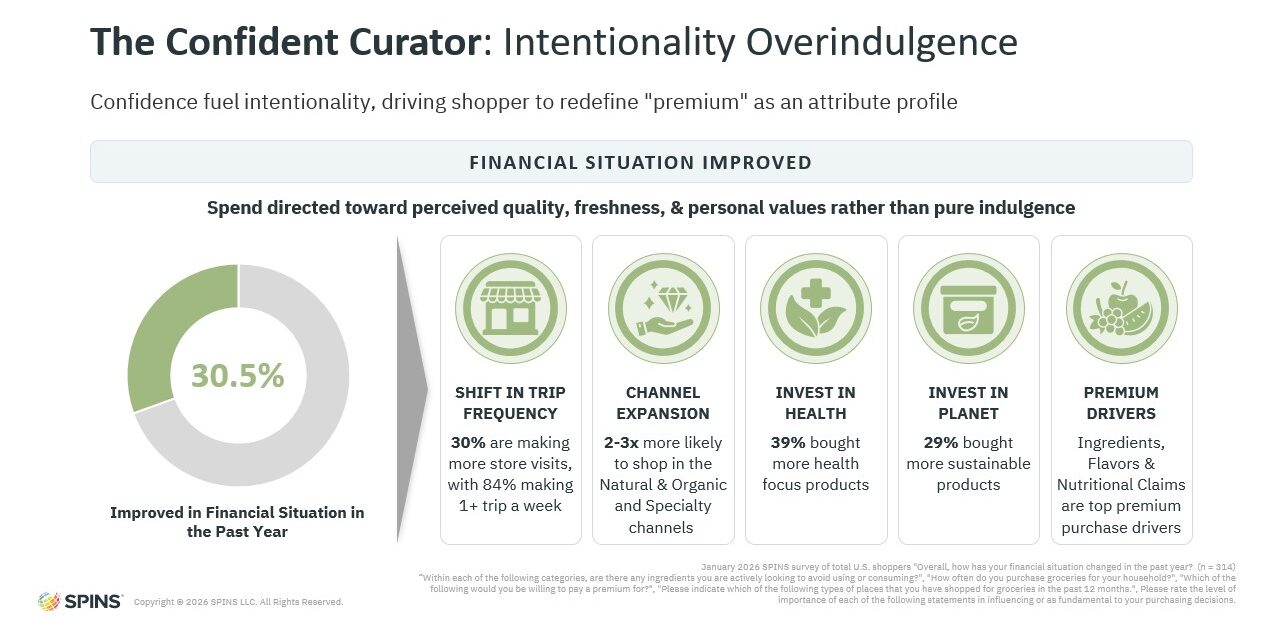

The Confident Curator: Intentionality Overindulgence

For the one-third of consumers reporting improved financial standing compared to the year prior, confidence has fueled intentionality. These shoppers are redefining “premium” not as a price point, but as an attribute profile. An increase in perception of financial standing has fueled consumers to purchase items that are not only higher in price but also of higher quality.

- The Shift to Frequency: 30% of this cohort increased their overall store trips, with nearly 84% shopping multiple times per week.

- Channel Expansion: They are diversifying away from one-stop stock-ups, leaning disproportionately into Natural & Organic and Specialty channels to curate specific items.

- Attribute-First Loyalty: Brand loyalty is being replaced by attribute loyalty. Over 29% increased their purchase of health-focused and sustainable products, proving that for this group, value is a blend of transparency, wellness, and clean ingredients.

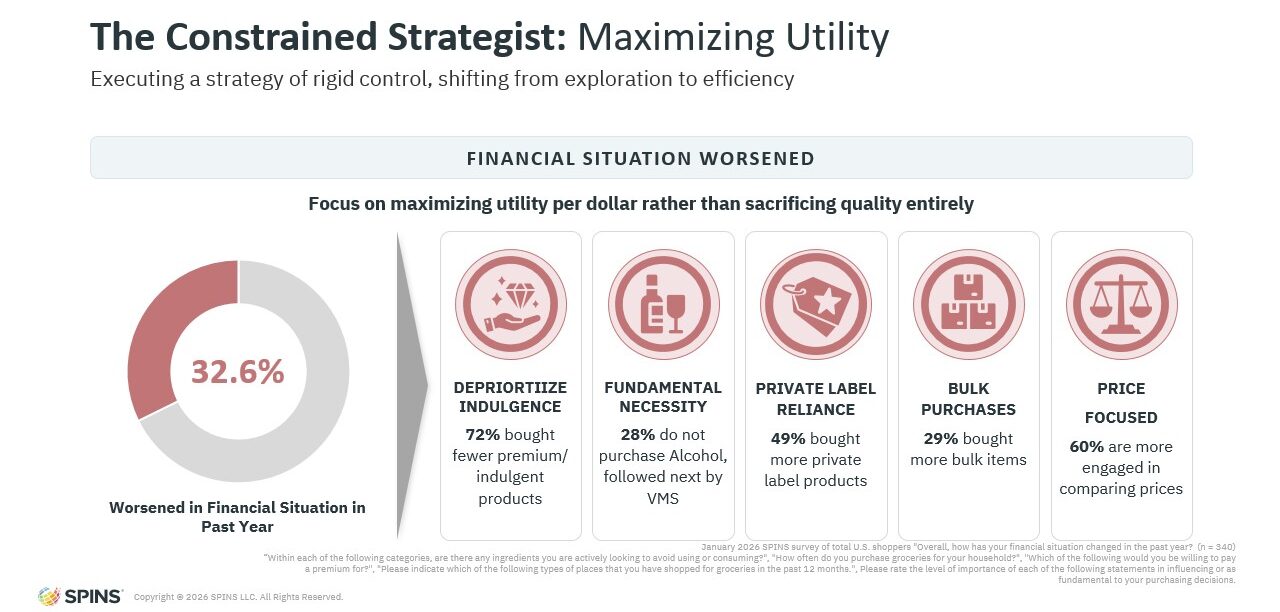

The Constrained Strategist: Maximizing Utility

Conversely, consumers facing financial headwinds are executing a strategy of rigid control. Their behavior shifts from exploration to efficiency.

- Consolidation: They are making fewer trips (43% decrease) to reduce impulse exposure.

- The Value Toolkit: This group is pulling multiple levers to maximize utility per dollar: increasing Private Label reliance (49%), buying more in Bulk (29%), and aggressively hunting Promotions (57%).

- Functional Necessity: Scrutiny of ingredient labels has decreased in favor of price comparison (60% increase in engagement). Here, the decision hierarchy prioritizes the shelf price over the ingredient deck.

Part II: The Attribute of Ethics

From Mission Statements to Measurable Impact

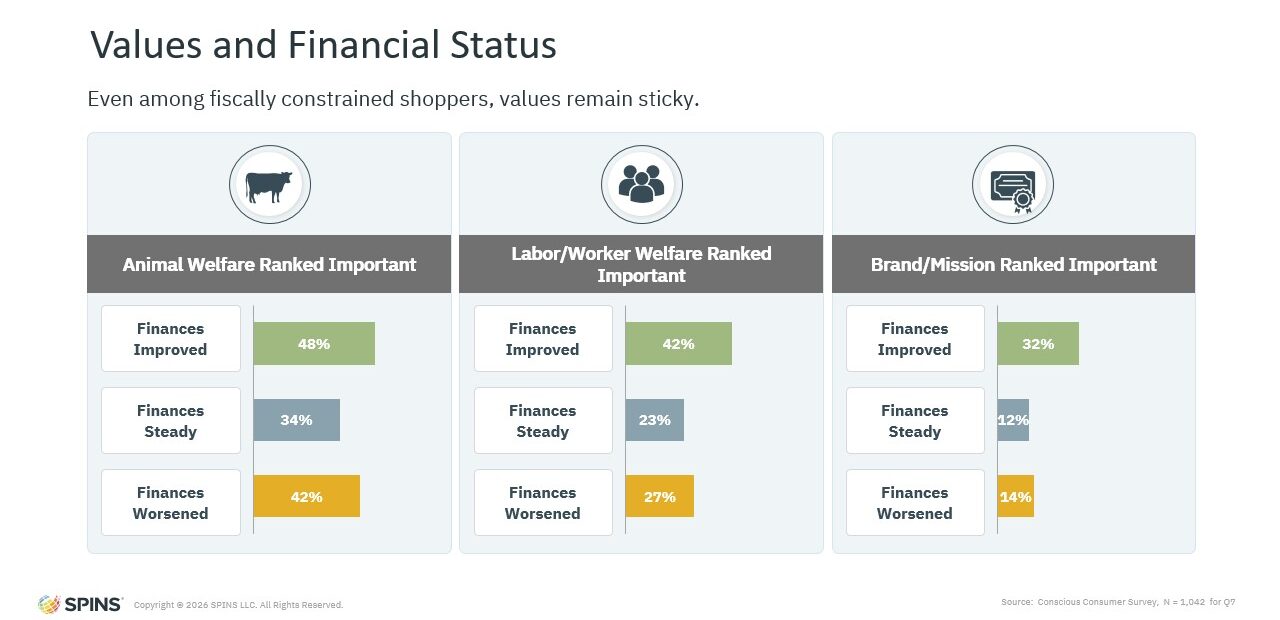

Despite economic pressures, values-based decision-making remains resilient. However, the data reveals a critical hierarchy: shoppers are prioritizing tangible impact over corporate philosophy. Concrete welfare claims are significantly outperforming abstract mission statements.

The Hierarchy of Values

- 40% of shoppers rank Animal Welfare as a top priority.

- 30% prioritize Labor/Worker Welfare.

- Only 19% rank a generic Brand Mission as a primary driver.

This signals a clear mandate: Shoppers want to verify the action (e.g., “Fair Trade,” “Free Range”), not just read the intent.

The “Grass-Fed” Proof Point

These sentiments are converting to volume at the shelf. The Grass-Fed attribute serves as the prime indicator of this shift:

- Penetration: 38% of households purchased a Grass-Fed item in the last 52 weeks, a 5% increase YOY.

- Velocity: Units are up 27% YoY, with dollar sales jumping 37%.

Crucially, the gap in prioritizing Animal Welfare between financially “improved” and “worsened” households is a mere six points. Even among constrained shoppers, values remain sticky. For many shoppers, ethical attributes are now considered a standard of quality, not a luxury add-on.

Part III: The Structural Shift in Private Label

Beyond the Recessionary Stopgap

The “Constrained Strategist” has catalyzed a permanent evolution in store brands; Private label brand purchasing is no longer just a recession story—it is a story connecting a structural shift in shopper behavior. While household penetration is nearly universal, growth is being driven by distinct demographic cohorts rather than only financial standing.

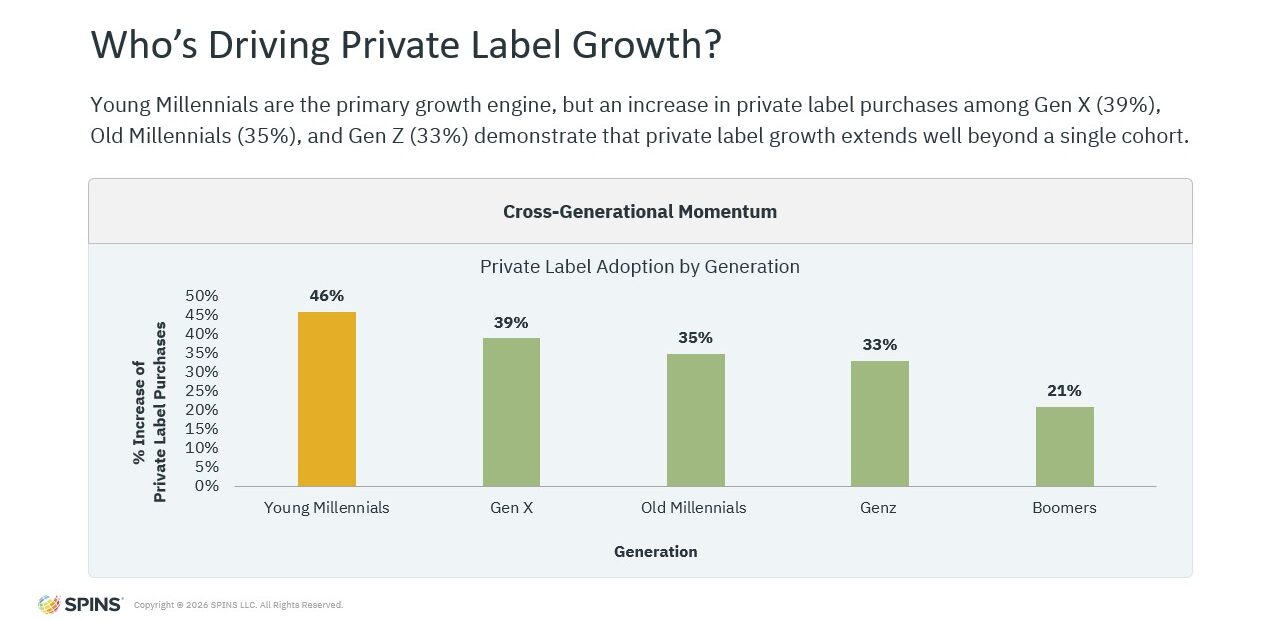

The Generational Hand-Off

As Gen Z and Millennials establish independent households, they are actively redefining the basket. When looking at Private Label items, millennials are driving volume in functional staples like Refrigerated Eggs, Frozen Proteins, and Household Products. Simultaneously, Gen Z is fueling dollar sales growth in core categories within Private Label, such as Milk, Bread, and Refrigerated Cheese—specifically outpacing national brands in attribute-rich segments like Plant-Based.

Affluence & Choice

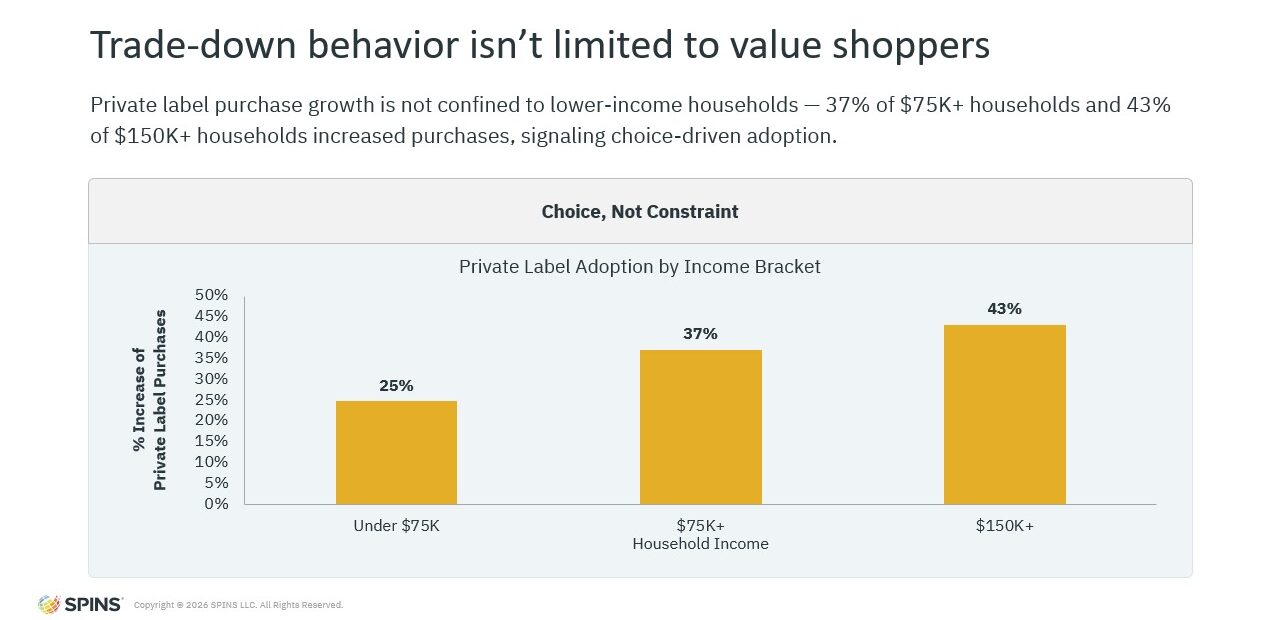

The data dismantles the “trade-down” myth. Increased private label engagement is now driven by choice, not just constraint:

- 43% of households earning over $150K increased their private label spend.

- 37% of those earning over $75K followed suit.

Store brands now compete on trust, quality, and attributes. For national brands, the answer is not deeper discounting—it is sharper differentiation and innovation that justifies the premium on shelf.

Part IV: The Mechanics of Discovery

Universal Trial & The Fragmented Path

Brand trial is now universal. With 94% of shoppers purchasing a new brand in the past year, loyalty is no longer a default state but rather a cycle of constant re-acquisition. However, the “trigger” for that trial has fractured across generational lines, creating a dual economy of discovery – one that prefers analog and another that prefers discovering digitally.

The Channel Divide

While the Search Bar has become the universal online tool for 63% of all product research, the initial discovery phase holds a sharp demographic split:

- The Analog Anchors (Boomers & Gen X): These cohorts remain tethered to the physical store. Their discovery is driven by In-Store Promotions, Sampling, and Grocery Ads.

- The Digital Natives (Gen Z & Millennials): This group has integrated the feed. Gen Z significantly under-indexes on traditional ads, with 54% citing Social Media as their primary influence. For them, discovery is leaning into their algorithms. Though AI as a discovery tool is still nascent, MikMak customers have seen more than a 30x rise in ChatGPT referral traffic since January 2025

The Attribute Trigger

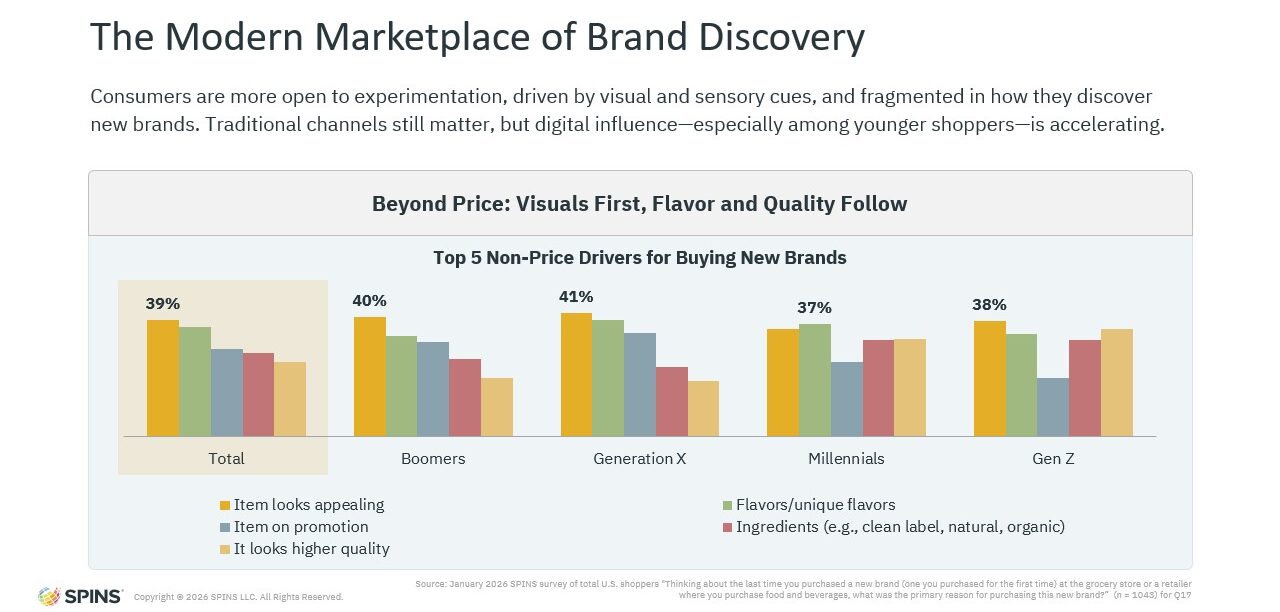

Once a product is discovered, outside of price, specific attributes tip the scale:

- Visual & Sensory Appeal: Across all generations, Visual Appeal (39%) and Unique Flavor Profiles (29%) are the top drivers of trial, with Ingredients floating among the Top 5 reasons.

- Millennials: This cohort is most likely to be swayed by Label Claims, Certifications, and Functional Ingredients.

- Gen Z: They are heavily influenced by Sustainability and Sourcing Claims, signaling that for the next generation, ethical impact is a key component of quality.

Conclusion

The Contextual Imperative

Across these numerous shifts, one theme is undeniable: conscious consumption is not replacing value; it is redefining it. Shoppers are still managing budgets, but they are doing so with sharper priorities, using a matrix of ingredients, ethics, and relevance to determine what is “worth it.”

The End of the Monolith

The era of the single “consumer mindset” is over. Purchasing decisions are now deeply contextual, shaped by the intersection of financial sentiment, life stage, and personal values. The winners will be those who recognize this context and build assortments that help shoppers feel confident they are buying in alignment with what matters to them now.

Data Sources

SPINS Trilens Panel (Powered by Circana), 52 weeks ending December 28, 2025

January 2026 SPINS Survey, Conscious Consumption: How Values Shape the Basket (N = 1,043)