Over the past several years, the CPG industry has weathered a seemingly consistent barrage of economic “shocks” to the system – some real, some perceived. These shocks have a cumulative effort, resulting in a general sense of uncertainty and disruption that permeates decision-making.

At SPINS, we are deeply invested in our customers’ businesses and relentlessly committed to supporting decisions with an evidence-based view of the industry and ecosystem; this is central to our ethos of partnership and community.

So over the next few months, SPINS will release a series of briefs highlighting well-known ingredients and how supply chain or cost disruptions have worked their way through to consumers, if at all. We will also look at how demand has shifted in response to price changes.

Why ingredients? Ingredients are often the first line of impact in macroeconomic disruptions and can provide a helpful proxy for understanding the downstream implications of global phenomena.

In our first spotlight, we focus on a category whose core commodity has seen an impact on price due to both tariffs and crop yields – Chocolate (specifically, Baking Chocolate)

The following data comes from SPINS Total US Natural Expanded & Mulo +Conv (Powered by Circana) Point of Sale data and SPINS TriLens Panel, Total US – All Outlet (powered by Circana).

Market Pricing

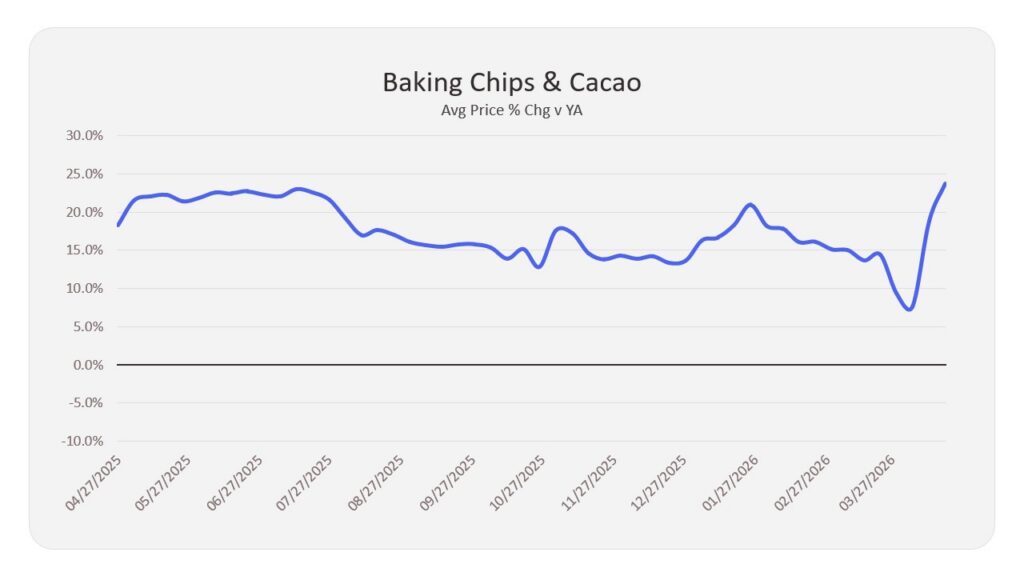

Baking chocolate feels the heat

Despite Grocery inflation being a major news story over the past few years, very few categories have increased prices as much as Baking Chocolate. Despite a very slight decline in the rate of those increases in 2026, category-wide prices are still up double digits vs this time last year, and have been at that elevated level consistently over the last 12 months (see Exhibit 1). While there was briefly some relief for consumers when compared to the 20%-30% price increases of early 2025, the 15.6% YoY increase in 2026 is significantly higher than what most consumers are used to seeing, and those increases have spiked again in the last month.

Exhibit 1:

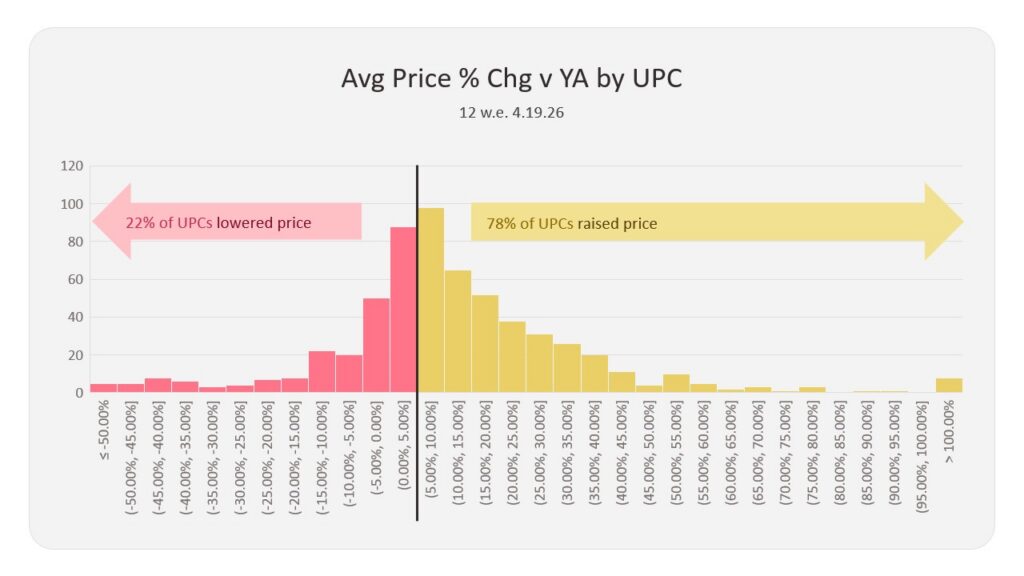

Furthermore, category shoppers are having trouble insulating themselves from higher prices in the category; The vast majority of UPCs on shelf have raised price vs year ago (see Exhibit 2). Unlike other categories, this is not a case where higher prices are the result of shoppers trading up to new and more premium products. In fact, most shoppers are finding that the products they are used to seeing on store shelves are getting more expensive, many by double digits.

Exhibit 2:

Demand Impact

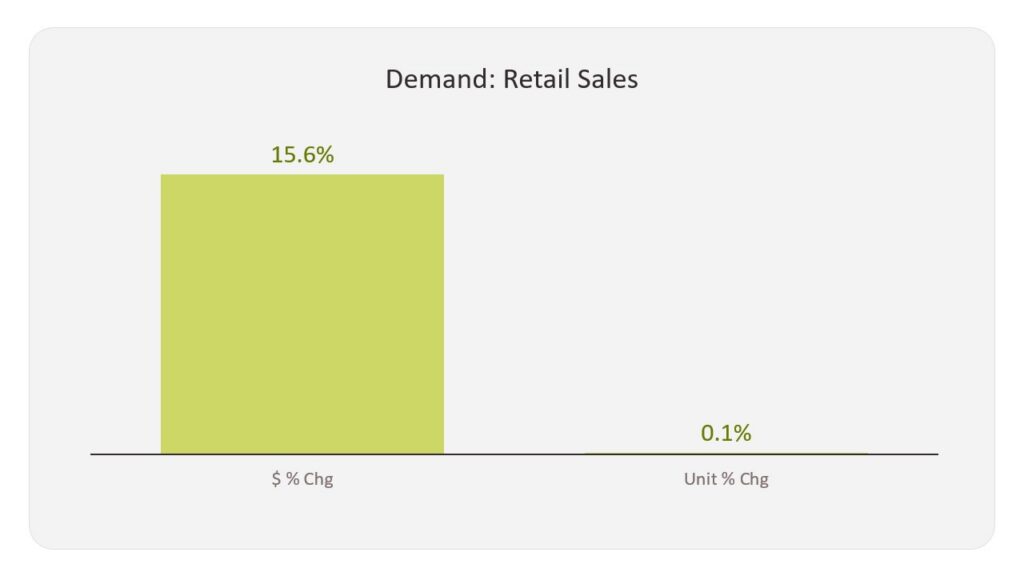

Loyal to the chocolate core

Despite consistent price inflation, consumers are not leaving the category en masse. Units are flat at +0.1% across the category, while Household Penetration is also up 0.6 pts vs the previous year (see Exhibit 3). Despite consistent double-digit price increases across most of the category, the category is attracting more consumers, and those consumers are buying more than ever.

Exhibit 3:

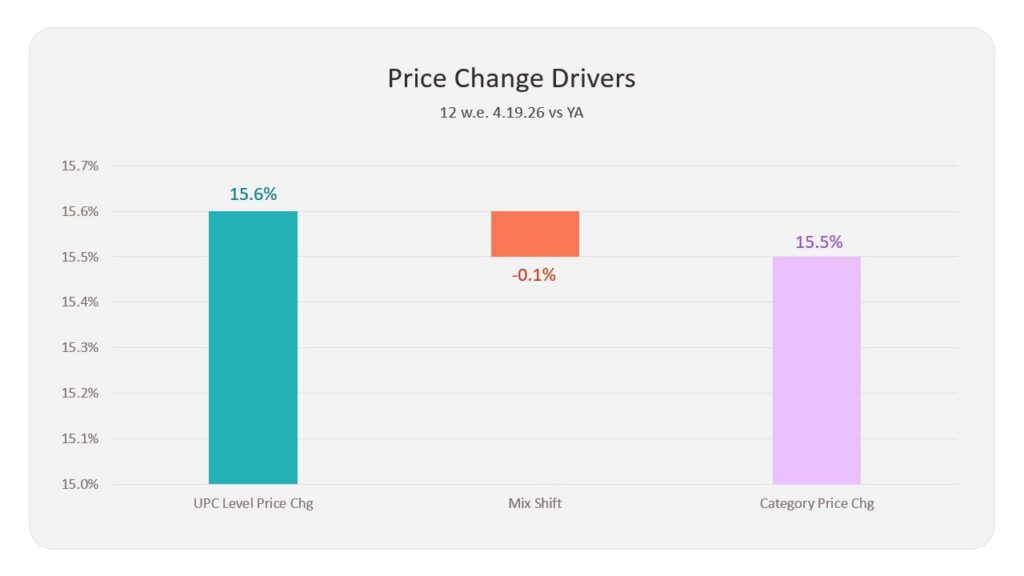

Some shoppers are responding to higher prices by staying in the category but trading down to less expensive items. While the average price for the entire Baking Chips and Cacao category is up 15.6%, the price for the average product in the category is up 15.5% (see Exhibit 4), meaning shoppers are responding by trading down to less premium, lower-priced products.

Exhibit 4:

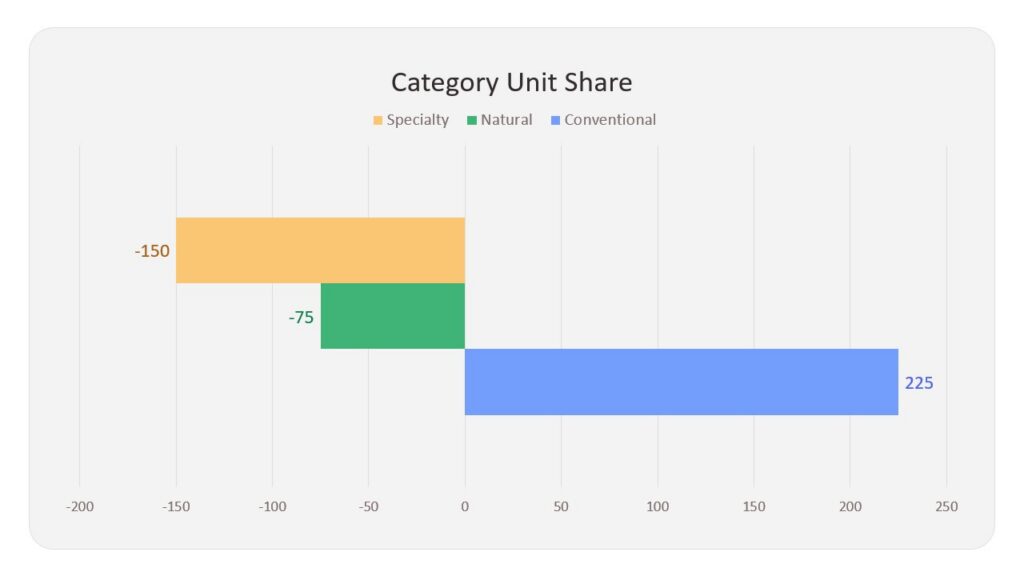

That trade-down strategy that some consumers are employing has been good for more mainstream and value-priced products. As higher-priced Natural and Specialty-positioned products gain share across most grocery categories, in Baking Chips & Cacao, we’ve seen a big swing towards lower-priced, conventionally positioned products. This swing has also been a boon for retailers’ own brands, as the Private Labels share in the category has increased by 0.7 share points vs the previous year, up to 33.1% of unit sales over the last 12 weeks (see Exhibit 5). Retailers have also been able to take advantage of organic shoppers’ willingness to trade down in price, as Organic Private Label products have grown 1.4 share points vs the previous year.

Exhibit 5:

Impact and resilience are an excellent pairing

Overall, the rapid and broad-based price increases and the surprising resiliency we see in overall category demand show how some categories are irreplaceable staples. These categories, though impacted by higher costs, have raised prices to consumers while maintaining overall demand. Consumers are responding, with some shifting down to lower-priced products, but demand for the category is high enough, and overall category elasticity is low enough, that Baking Chips and Cacao have so far been able to weather the storm and maintain sustained demand and healthy growth.

Downloadable Chart Pack

Access the individual slides shown in this post — formatted and ready to use in your own presentations.