Introduction

The first thing attendees encountered stepping off Katella Avenue wasn’t a supplement brand or an organic snack startup. It was Steak & Shake, handing out free samples of beef tallow French fries. That detail alone set the tone for what Expo West 2026 turned out to be: a show shaped as much by shifting regulatory and cultural currents as by the brands themselves.

The overarching theme was shopper-first. Ingredients, certifications, and brand stories were intentional — built for today’s consumer rather than for aspirational lifestyle positioning. Messaging kept it simple: focused on what was and wasn’t in products, and why that mattered. Approachability was the point. Access to wellness, the show signaled, is for everyone. For a full look at everything SPINS captured on the floor, download the complete 2026 Expo West Recap here.

What was hot on the floor:

- Energy drinks with layered formulations

- Kosher and Halal certifications

- Clear protein beverages

- Creatine in every format imaginable

- Real dairy making a visible return at the expense of plant-based alternatives

What held steady:

- Regenerative organic

- Protein expanding across every aisle

- Seed oil aversion

- Whole grains having a cultural moment

- Women’s focused wellness and digestive health

What’s coming:

- Clean Label Purity Awards

- Climate Label certifications

- Non-UPF Verified claims

- Whey protein alternatives gaining traction as supply tightens

- Collagen evolving beyond beauty

- Diverse fiber sources finding new product homes

For a full look at everything SPINS captured on the floor, download the complete 2026 Expo West Recap here.

Here’s what SPINS saw across the floor.

Ingredient Shakeup: A Return to Real

Consumer skepticism about artificial ingredients has been building for years, but 2026 brought a new accelerant: a federal regulatory environment that is actively skeptical of the same ingredients shoppers have been questioning.

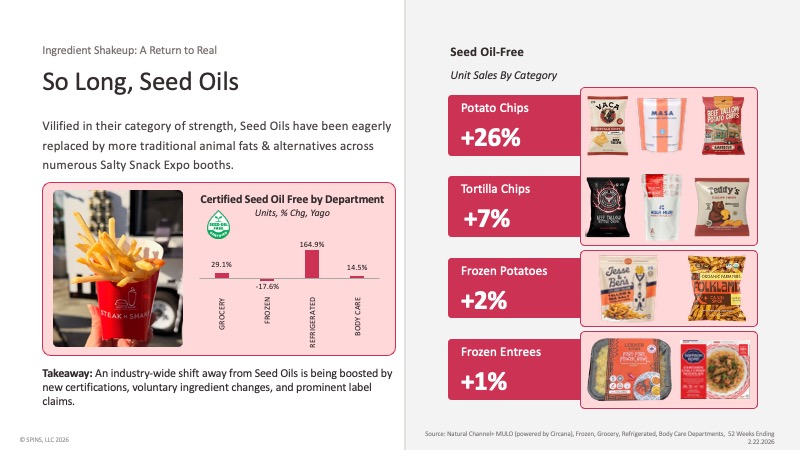

Seed oils are losing shelf space fast

The conversation around seed oils has migrated from wellness forums to mainstream grocery shelves, and brands are responding with reformulations, new certifications, and label claims that would have seemed niche just two years ago. The Seed Oil Free Certification has been around since 2023, predating the current administration, but it’s gaining momentum now that cultural and regulatory headwinds are aligned.

SPINS data from the 52 weeks ending 2/22/2026 shows seed oil-free potato chips up 26% in unit sales, tortilla chips up 7%, and frozen entrees up 1% — all small numbers in isolation, but notable given how recently the certification launched and how limited the certified universe still is. At Expo, salty snack booths were the most visible arena for this shift, with tallow-forward brands like VACA, MASA, and Ranger leading the charge. In Frozen, Jesse & Bens leaned into beef tallow while Folkland went simple with olive oil. Lekker Kitchen launched outright with a seed oil-free claim; Saffron Road revamped its entire product line to eliminate them.

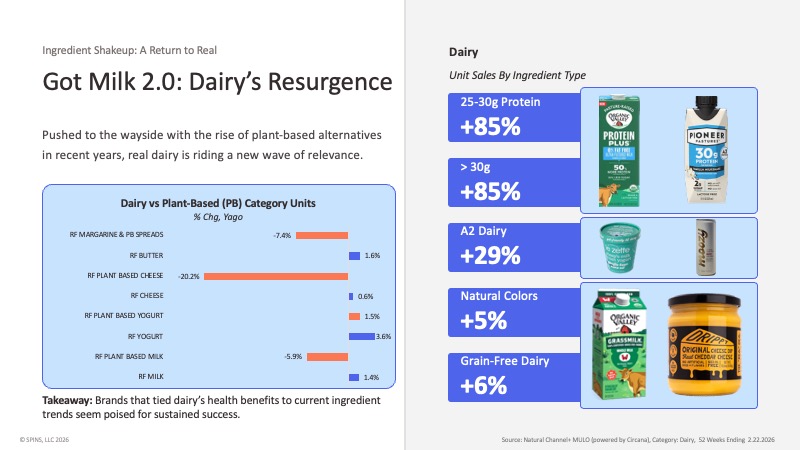

Real dairy is having a moment

For much of the past decade, plant-based alternatives dominated the dairy conversation at natural products shows. That dynamic has shifted. Consumers are returning to real dairy — not out of nostalgia, but because the protein boom and clean label movement have made conventional dairy, with its short and recognizable ingredient list, suddenly look like a better option than its alternatives. The data backs it up. Plant-based dairy has been in retreat across the refrigerated case — plant-based milk down 5.9%, plant-based cheese down 20.2%, plant-based yogurt down 7.4% — while conventional dairy holds steady or grows.

Brands at Expo were leaning into three angles: high-protein dairy (units up 85% for products in the 25–30g range, same growth for 30g+), A2 formulations (up 29%) for consumers who love dairy but struggle to digest standard A1 proteins, and clean label claims that go beyond antibiotic-free to include grain-free, no artificial colors, and pasture-based sourcing. Organic Valley’s Grassmilk and Pioneer Pastures were among the standouts; Le Zette and Moozy made a case for A2 as a broader audience play.

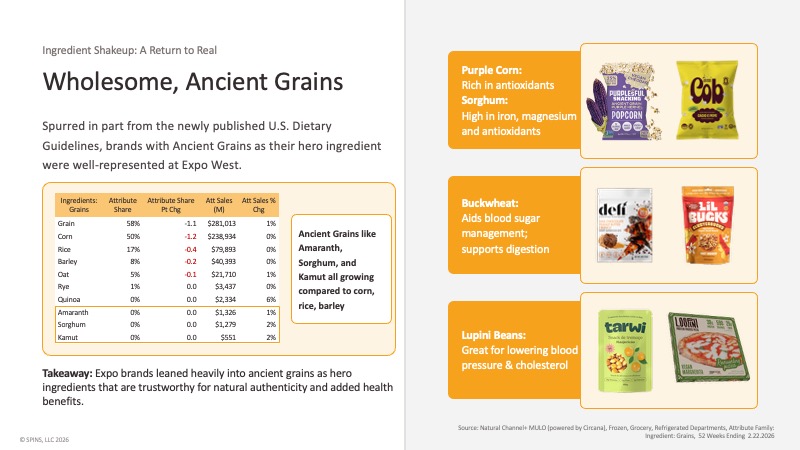

Ancient grains found their moment

Whole grains have long lived in the background of the natural products aisle – present, but rarely the hero of the story. That changed this year. The newly updated U.S. Dietary Guidelines put a specific emphasis on whole grain consumption, and brands took that opening. The framing at Expo wasn’t “healthy” in the abstract, but rather, it was these plants that have been consumed for centuries. Purplesful Snacks are built around purple corn, rich in antioxidants. Cob Popcorn led with sorghum. Defi Snacks are centered on buckwheat. Tarwi and Loopini offered lupini as a dual protein-and-fiber play. In SPINS data, amaranth, sorghum, and kamut are all growing relative to corn, rice, and barley — still small in absolute dollars, but directionally clear.

Short Supply, Smart Swaps

Not every trend on the show floor was driven by consumer preference. Two significant supply-side pressures are forcing brands to rethink their formulations in ways that will ripple through product development for the next several years. Ingredient trends don’t happen in a vacuum, and these two dynamics signaled that adaptability is no longer optional.

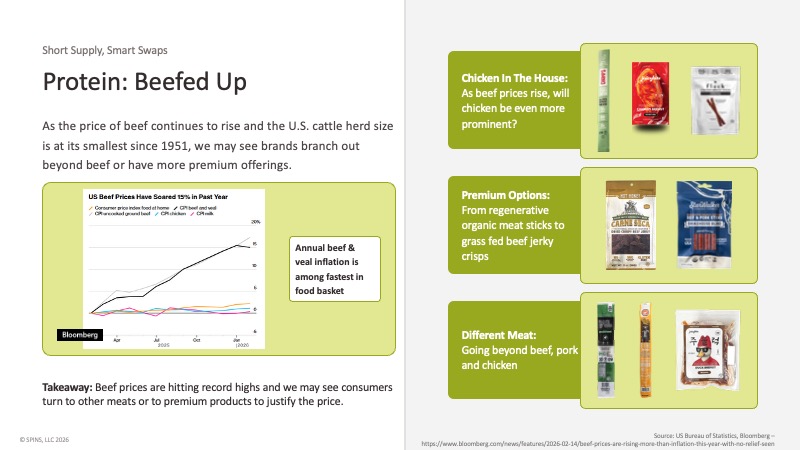

Beef prices are at record highs, and the U.S. cattle herd is at its smallest since 1951

That math is showing up in product development. High protein products continue to see strong growth, and we see chicken becoming more prominent in the meat snacks and jerky space as beef prices rise. However, we shouldn’t forget that despite the rising prices, consumers will still buy beef products. Premium beef products are also finding buyers willing to pay up: regenerative organic meat sticks and grass-fed beef jerky crisps were both present, suggesting consumers won’t abandon beef entirely but are increasingly looking for a reason to justify the price.

We saw game meats and other meats out on the show floor, again, another sign of diversification in the meat snacks space. For on-the-go meals, products like packaged chicken breast could grow in popularity as they already have in other regions like Asia

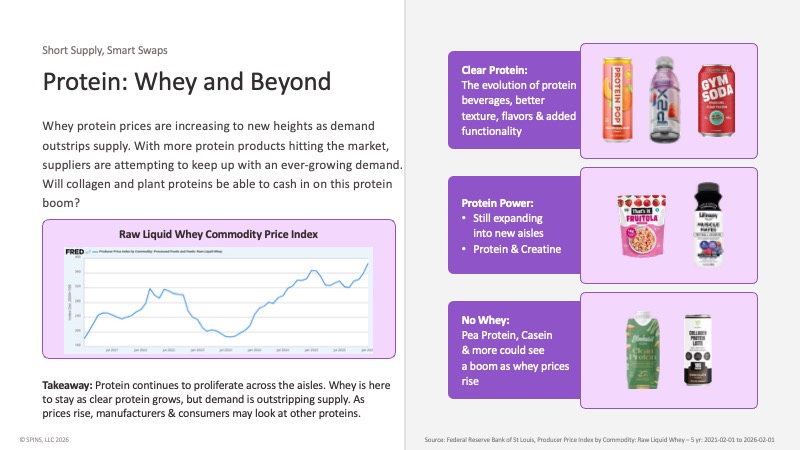

Whey protein demand is outstripping supply

Protein’s expansion across the store has been one of the defining CPG stories of the past few years. Now the infrastructure is straining to keep up. The Raw Liquid Whey Commodity Price Index has climbed to new highs, which is starting to open the conversation around alternatives.

Clear protein drinks continued to show up strong on the floor — improved texture, new flavor profiles, and functional additions like caffeine and electrolytes. Protein is also continuing to colonize new aisles: cereal, ice cream, chips, and yogurt are all fair game. The ingredient pairing gaining the most traction is protein plus creatine, which will come up again in the VMS section. As whey prices stay elevated, pea protein, casein, and collagen are the logical beneficiaries — though none have yet seen the kind of growth whey has.

2026 Trend Predictions

Energy Uncapped: Crafted Clean

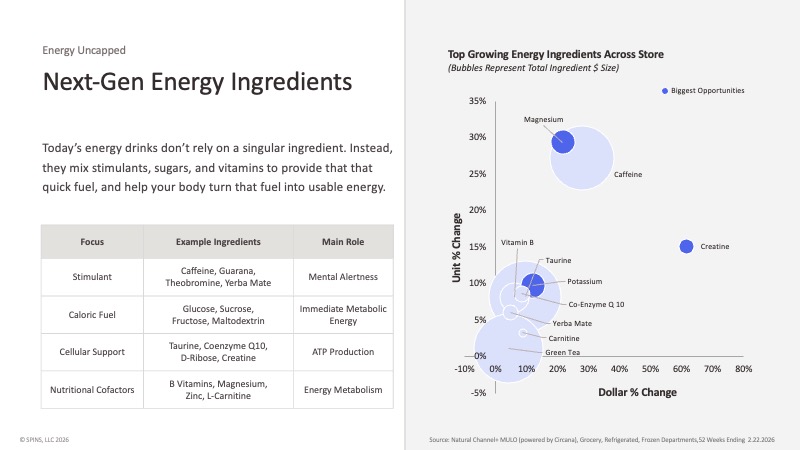

Energy has been one of the fastest-growing categories in natural products for the past several years, but the way brands are competing within it has fundamentally changed. It’s no longer a race to the highest caffeine count. Consumers are rewarding complexity, with formulations that deliver sustained performance rather than a spike and a crash.

The category has moved from single-source stimulation to multi-functional stacks. Formulations are now built across four roles: stimulants for alertness, caloric fuel for quick energy, cellular support (taurine, CoQ10, creatine) for sustained output, and nutritional cofactors like B vitamins and magnesium to help the body process it all.

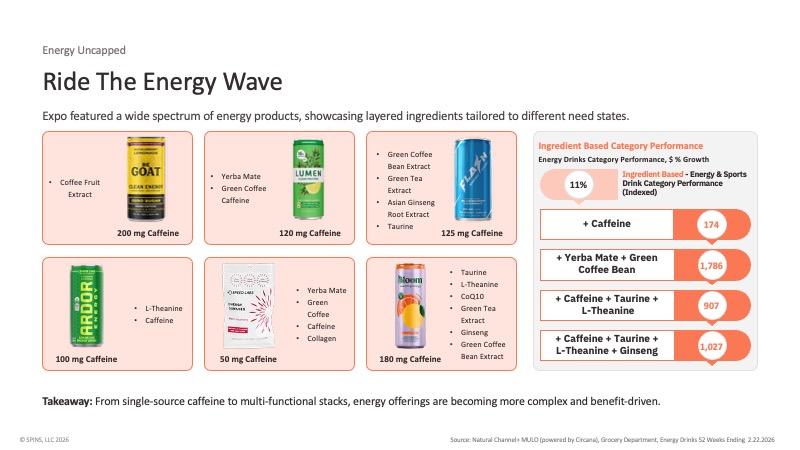

SPINS data indexed against the energy category’s 11% growth shows products layering caffeine with yerba mate and green coffee bean at 1,786 — and stacks adding taurine and L-theanine above 900. The numbers tell the story: complexity is outperforming simplicity.

BeGOAT, using coffee fruit extract for 200mg caffeine with a minimal ingredient list, represents the clean and simple end. Bloom Nutrition, blending caffeine with taurine, L-theanine, green tea, CoQ10, ginseng, and green coffee bean extract at 180mg, represents the stacked end. Both found space on the floor.

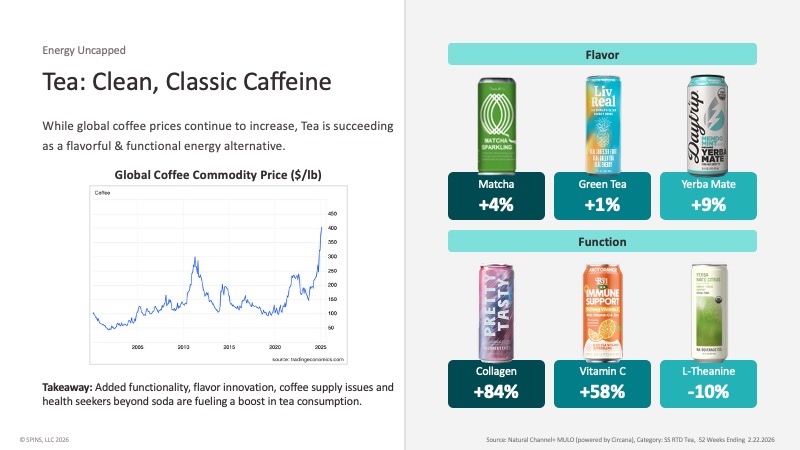

Tea is positioning itself as the post-soda energy alternative

Last year’s show told a clear story about the rise of functional sodas. In 2026, that category didn’t disappear, but it ceded the spotlight to something older and arguably better-positioned for what consumers are asking for right now: canned tea. The case for tea is both cultural and structural — clean caffeine, functional versatility, and a growing cost advantage as global coffee commodity prices continue to climb.

Spindrift and Daytrip both announced entry into the RTD tea category at the show. St. James and Just Iced Tea expanded their lines. Functional tea is growing fastest in collagen (+84%), and Vitamin C (+58%) — and brands like Pretty Tasty (collagen-infused), Liv Real (green tea caffeine paired with L-theanine and electrolytes), and The Ryl Tea Co (500mg Vitamin C immune support line) are already making the functional play.

Certifications, Practices & Initiatives

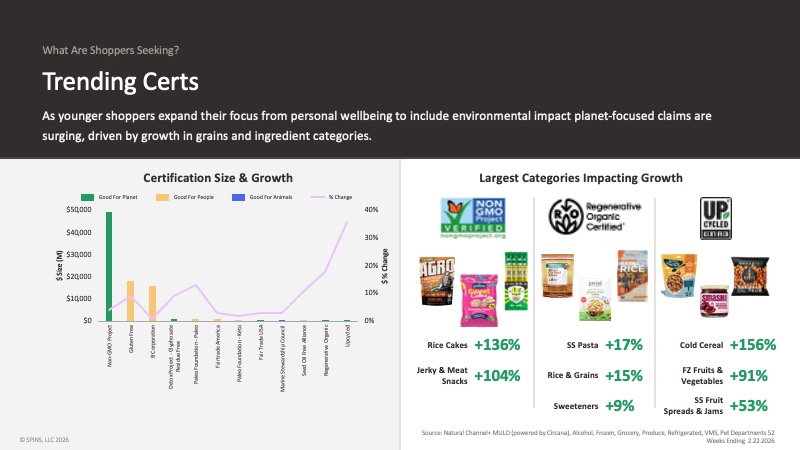

Third-party certification has always been a feature of the natural products channel, but what brands are choosing to certify — and why — is shifting. The conversation has moved beyond organic and non-GMO into more specific claims about sourcing, processing, environmental impact, and ingredient purity. Across the show floor, certifications weren’t just labels. They were central to how brands told their stories.

Six certifications showed up with meaningful frequency, each addressing a different dimension of consumer skepticism. Regenerative Organic Certified goes beyond the organic standard to verify healthy soil, animal welfare, and social fairness throughout the supply chain. The Clean Label Purity Award tackles verified low levels of contaminants, including heavy metals, pesticides, and plasticizers. The Climate Label Certified requires brands to transparently measure, reduce, and report their greenhouse gas emissions. Non-UPF Verified confirms that a product contains minimally processed ingredients and excludes highly processed additives. The Soil & Climate Initiative supports regenerative farming practices with a specific focus on soil health, biodiversity, and lower emissions. And Kosher and Halal certifications showed up as one of the show’s hottest signals — reflecting both the growing purchasing power of observant consumers and a broader interest in third-party verification of ingredient integrity.

Non-GMO Project still leads in certified-product dollar size by a wide margin. But regenerative organic and upcycled are among the fastest-growing, and the categories driving that growth are telling: cold cereal up 156% in regenerative organic certified sales, rice cakes up 136%, frozen fruits and vegetables up 91%, jerky and meat snacks up 104%.

Lundberg was a standout — not only Non-GMO but regenerative organic, with Sweet Cakes made from certified brown rice in facilities powered by 100% renewable energy. Big Tree Farms, working with over 19,000 farmers across coconut sugar, cacao, and spices, represented the supply chain transparency angle. Smash Foods represented the upcycled angle, using “imperfect” fruits and chia seeds to produce jam with a fraction of the conventional sugar load.

Gut Instincts: The Mighty Microbiome

Digestive health has been a consistent category driver in natural products for years, but the science and the consumer conversation around it are both evolving. Gut health is no longer just about probiotics and digestive enzymes. Research increasingly connects the microbiome to mood, cognitive function, and systemic wellness — and that broader framing is showing up in how brands formulate and how consumers shop.

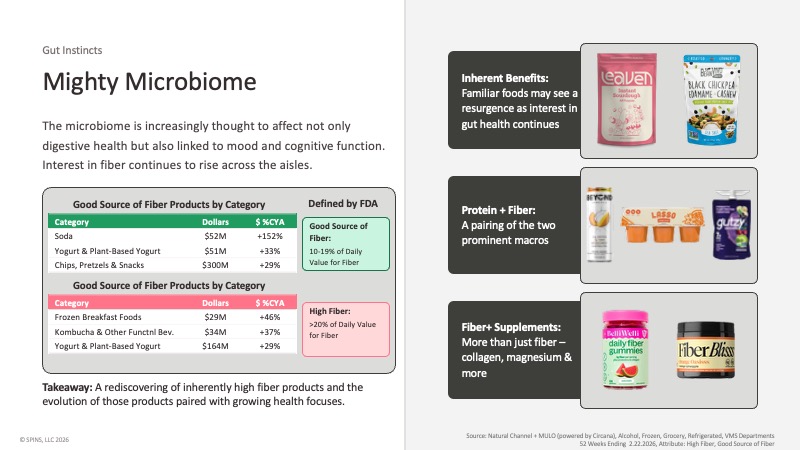

Digestive health has expanded well beyond probiotics. Interest in fiber, in particular, is rising across every aisle — and not just in the supplement section.

In SPINS data, “good source of fiber” products (10–19% daily value) are growing fastest in soda ($52M, +152%), yogurt and plant-based yogurt (+33%), and chips, pretzels, and snacks ($300M, +29%). At the high-fiber level (>20% daily value), the top three growing categories are frozen breakfast foods (+46%), kombucha and other functional beverages (+37%), and yogurt (+29%). Yogurt appears in both tables, and it earns that position, delivering simultaneously on fiber and inherent probiotic content.

The other angle at Expo was fiber-plus supplements: products that deliver fiber alongside functional additions like collagen, magnesium, and other micronutrients. The protein-plus-fiber pairing is also gaining real momentum as consumers look to address both macros at once.

Chew, Glow, Go: The New Face of VMS

The vitamins, minerals, and supplements category has been in a period of rapid evolution — driven partly by new science, partly by cultural shifts in how people think about performance and aging, and partly by format innovation that is making supplementation more accessible and routine. At Expo, three stories dominated: creatine expanding well beyond the gym, collagen taking on a broader wellness identity, and women’s health finally getting the specificity it has long deserved.

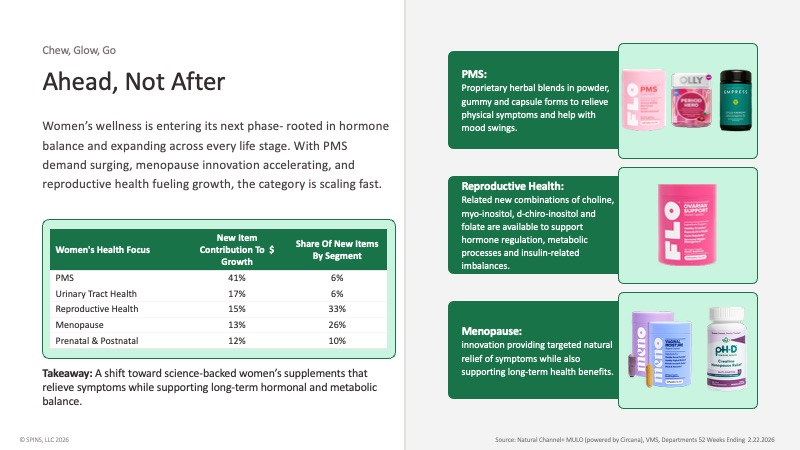

Women’s wellness is entering a new phase

The women’s health supplement category has historically been under-differentiated — multivitamins marketed to women, or reactive formulations for PMS and menopause. That’s changing. Brands are now building products around the full arc of women’s hormonal and metabolic health, and the growth numbers reflect how much unmet demand existed. Historically framed around PMS and menopause, the category is now addressing hormones, cycle tracking, reproductive health, and life-stage transitions in more targeted ways.

SPINS data shows PMS supplements contributing 41% of new item dollar growth in women’s health, with reproductive health (15%) and menopause (13%) also driving significant new item activity. On the floor, Empress Herbal Powders, FLO Reproductive Health, and PH-D Creatine Menopause Relief each showed how far the category has moved from generic women’s multivitamins.

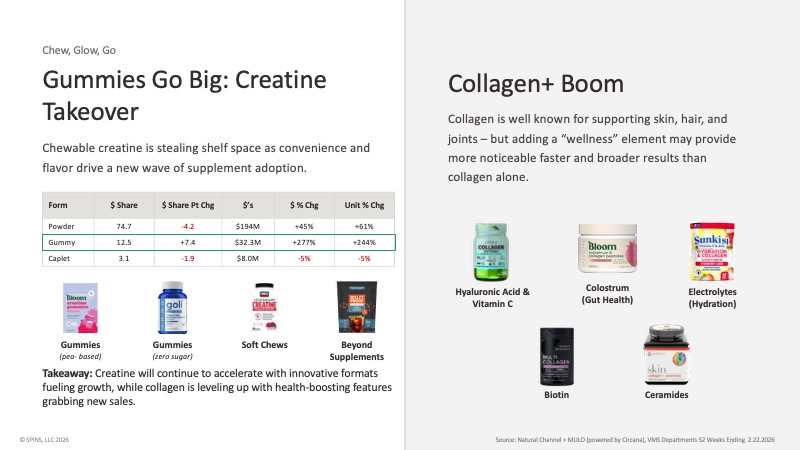

Creatine is everywhere — and leaving the supplement aisle

Creatine’s transformation from a niche sports supplement into a mainstream wellness ingredient has been one of the more interesting category stories of the past two years. What started in powder form for gym-goers is now appearing in gummies, soft chews, beverages, and combination products — and the consumer base has expanded well beyond athletes. Gummies are gaining share (+277% in dollar growth, +244% in units) while powders remain dominant at 74.7% dollar share but are losing share. Creatine is also going beyond the supplements aisle and entering the beverage aisle, a natural progression we see in the industry.

Collagen is leveling up

Collagen has been a fixture in the beauty supplement space for years, but the category is maturing into something broader. Single-benefit positioning — skin, hair, joints — is giving way to multi-functional formulations that stack collagen with other high-interest ingredients. The new positioning layers collagen with hyaluronic acid, Vitamin C, colostrum for gut health, or electrolytes for hydration — moving it from a beauty ingredient to a broader wellness play.

The Arnold Sports Festival, running the same week as Expo, reinforced the active nutrition side of this story. Performance has extended beyond muscle and joint support to include glucose management, liver health, sleep, and stress. Peptides and nootropics were active conversations on the floor, and the trend toward format innovation — strips, pouches, mists, waterless creatine — shows the category is optimizing for compliance as much as efficacy.

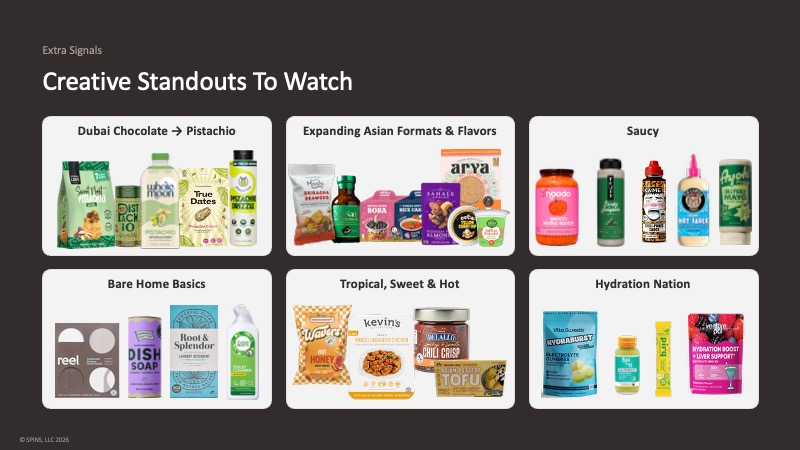

Extra Signals Worth Watching

Not every trend at Expo fits neatly into a category narrative, but several standouts are worth tracking for what they signal about where consumer interest is heading. Some are flavor-driven, some are format-driven, and some are simply cultural moments finding their way into the product.

Pistachio has outgrown the Dubai chocolate moment and is now appearing across condiments, snacks, and beverages as a mainstream flavor. Asian flavors and formats continue to see sustained consumer interest — from innovative chip flavors to clean-label takes on familiar formats. Swicy (sweet and spicy) is holding strong through mango habanero, hot honey, and chili crisp. Hydration has pulled back from triple-digit growth rates but remains in active innovation, with gummy formats, shots, and multi-functional powders that address liver support alongside electrolytes.

SPINS at Expo West 2026

Beyond tracking what was on the show floor, SPINS brought its own data-driven perspective to Expo through a series of thought leadership presentations. If you weren’t in Anaheim, the 2026 State of Industries: Natural, Beverage, and Supplements webinar brings key content from the stage directly to you — covering how the natural industry is performing, which categories and functional ingredients are driving growth in beverage and supplements, and how consumers are shopping across both. Watch it on demand now.

This year’s full slate of Expo presentations covered the breadth of the natural products landscape:

- State of Supplements 2026

- Analytics, Activations, and Agents: Using Data to Survive and Thrive in a 3-Shelf Reality

- State of Beverage 2026

- State of Active Nutrition 2026

- The Fiber Revolution

- Organic Market Trends and Insights

- Expectations of the Conscious Consumer

All seven presentations are available at explore.spins.com/expo-west-2026-thought-leadership.